On 14 May 2024, the Treasurer, Jim Chalmers, delivered his third Federal Budget for the Albanese Government. With an uncertain economic landscape with Australia continuing to face ongoing global uncertainty stemming from persistent inflation in North America; growth slowing in China and other major economies; the United Kingdom and Japan both finishing the year in recession; and ongoing wars in the Middle East and Eastern Europe.

Additionally the Australian economy, businesses and families are still feeling the devastation of floods and bushfires, a once-in-a-century global pandemic, followed by the most significant international energy crisis in decades. The combined impact of these events have resulted in significant supply chain delays and very large increases in energy prices, inflation and interest rates.

It is under these headwinds, the Budget was handed down with intent to offer cost of living relief and funding and spending focused on the following areas:

- Aged care

- Personal tax cuts

- Household and business energy bills rebates

- Reduction in cost of medicines

- Funding the flagship “Future Made in Australia” agenda. but contains little in the way of support for small business

This Budget is expected to deliver a surplus of $9.3 billion for the 2023/24 fiscal year, the first time the Budget has posted successive surpluses in two decades, but with forecast for deficits over the following four years.

We have summarised the key announcements we feel to be most relevant to the majority of our clients.

Personal income tax measures

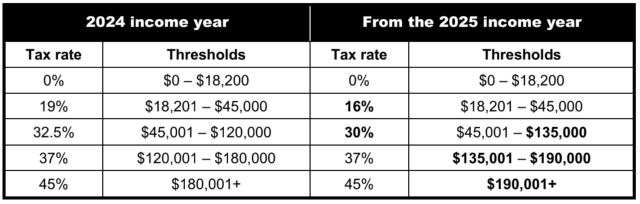

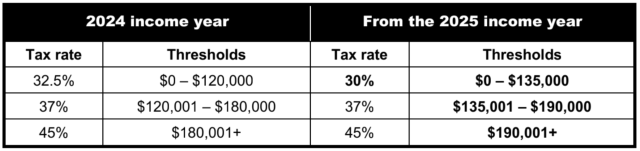

Stage three personal tax cuts

The Government has confirmed the revised stage three personal tax cuts that were announced prior to the Federal Budget being handed down and which have already been enacted into law.

The following tables outline the marginal income tax rates and thresholds that apply for resident and foreign resident individuals under the revised stage three personal tax cuts from 1 July 2024 (i.e., from the 2025 income year).

The tax rates and thresholds that apply for the 2024 income year are included for comparative purposes.

Australian resident individual income tax rates

Foreign resident individual income tax rates

Small business measures

Temporary increase to the instant asset write-off

Under current law, the small business instant asset write-off threshold is (less than) $1,000 for the

2025 income year. However, the Government has announced that it will temporarily set the instant asset write-off

threshold for small business entities at (less than) $20,000 for the 2025 income year. This was originally set to end at 30 June 2024.

The means small businesses with an aggregated annual turnover of less than $10 million will generally be able to immediately deduct the full cost of eligible assets costing less than $20,000 that are first used or installed ready for use by 30 June 2025. The asset threshold applies on a ‘per asset’ basis, so small businesses can instantly write off multiple assets.

Assets valued at $20,000 or more (i.e., which cannot be immediately deducted) can continue to be placed into the small business simplified depreciation pool and depreciated at 15% in the first income year and 30% each income year thereafter. The provisions that prevent small businesses from re-entering the simplified depreciation regime for five years if they opt-out will continue to be suspended until 30 June 2025.

From 1 July 2025, the instant asset write-off threshold will revert back to (less than) $1,000.

Retaining Business Activity Statement (‘BAS’) refunds

The Government will strengthen the ATO’s ability to combat fraud by extending the time the ATO has to notify a taxpayer if it intends to retain a BAS refund for further investigation. The ATO’s mandatory notification period for BAS refund retention will be increased from 14 days to 30 days to align with time limits for non-BAS refunds.

Legitimate refunds will be largely unaffected. Any legitimate refunds retained for over 14 days would result in the ATO paying interest to the taxpayer.

This change will have effect from the start of the first income year after Royal Assent of the enabling legislation.

Relieving energy bill pressures

The Government is providing certain direct energy bill relief for small businesses. Of note, the Energy Bill Relief Fund is providing energy rebates to each of the approximately one million businesses on small customer electricity plans to help cover their electricity bills. This Budget will provide additional energy bill relief of $325 to eligible small businesses.

Expanding the Digital ID System

The Government is expanding the Digital ID System. The expanded system will lower the

administrative burden on small businesses by reducing the amount of ID data they need to store

and protect for their customers and their employees.

Building cyber resilience for small businesses

The Government is supporting small businesses to be secure online while they adopt and harness digital opportunities, including through funding the following:

- Cyber Wardens program to provide free, online training for small business owners and their staff to help drive cultural change and a cyber safe mindset in Australian small businesses.

- Small Business Cyber Resilience Service to help small businesses build their cyber resilience and provide support when affected by a cyber incident.

- Cyber Health Check online interactive tool to enable small and medium businesses to self-assess their cyber security maturity.

- The Government is also developing a ransomware playbook to provide guidance on how to prepare for, respond to and recover from, a ransomware or cyber extortion incident.

Foreign residents

Strengthening the foreign resident CGT regime

The Government will strengthen the foreign resident CGT regime to ensure foreign residents pay their fair share of tax in Australia and to provide greater certainty about the operation of the rules.

The amendments will apply to CGT events commencing on or after 1 July 2025 to:

- clarify and broaden the types of assets that foreign residents are subject to CGT on;

- amend the point-in-time principal asset test to a 365-day testing period; and

- require foreign residents disposing of shares and other membership interests exceeding $20

- million in value to notify the ATO, prior to the transaction being executed.

This measure will ensure that Australia can tax foreign residents on direct and indirect sales of assets with a close economic connection to Australian land, more in line with the tax treatment that already applies to Australian residents.

The new ATO notification process will improve oversight and compliance with the foreign resident CGT withholding rules, where a vendor self-assesses their sale is not taxable real property.

Superannuation

Superannuation on Paid Parental Leave

The Government has announced that it will pay superannuation on Commonwealth government-funded Paid Parental Leave for births and adoptions on or after 1 July 2025. Eligible parents will receive an additional payment based on the Superannuation Guarantee (12% of their Paid Parental Leave payments), as a contribution to their superannuation fund.

Unpaid superannuation entitlements

The Government will recalibrate the Fair Entitlements Guarantee Recovery Program to pursue unpaid superannuation entitlements owed by employers in liquidation or bankruptcy from 1 July 2024.

Other budget measures

Energy bill relief for households

The Government is providing direct energy bill relief for every Australian household. From 1 July 2024, all households will receive a total rebate of $300, which will be automatically applied to their electricity bills in quarterly instalments. This rebate will not be means tested.

Discretion to not offset a refund against old tax debts

The Government has proposed to amend the tax law to give the Commissioner a discretion to not use a taxpayer’s refund to offset old tax debts, where the Commissioner had put that old tax debt on hold prior to 1 January 2017. This discretion will apply to individuals, small businesses and not-for-profits, and will maintain the Commissioner’s current administrative approach.

Extending ATO compliance programs

The Government has announced it will extend the following ATO compliance programs:

(a) Personal Income Tax Compliance Program

The Government will extend the ATO’s Personal Income Tax Compliance Program for one year from 1 July 2027. This extension will enable the ATO to continue to deliver a combination of proactive, preventative and corrective activities in key areas of non-compliance, including overclaiming of deductions, incorrect reporting of income and inappropriate tax agent influence. This will enable the ATO to continue its focus on emerging risks to the tax system, such as deductions relating to short-term rental properties.

(b) Shadow Economy Compliance Program

The Government will extend the ATO Shadow Economy Compliance Program for two years from 1 July 2026. This extension of the Shadow Economy Compliance Program will enable the ATO to continue to reduce shadow economy activity, thereby protecting revenue and preventing non-compliant businesses from undercutting competition.

(c) Tax Avoidance Taskforce

The Government will extend the ATO Tax Avoidance Taskforce for two years from 1 July 2026. Extending the Taskforce ensures the ATO continues to be well-resourced to pursue key tax avoidance risks, with a focus on multinationals, large public and private businesses, and highwealth individuals.

(d) ATO counter fraud measures

The Government will provide $187.0 million over four years from 1 July 2024 to the ATO to strengthen its ability to detect, prevent and mitigate fraud against the tax and superannuation systems. This will include funding:

for upgrades to information and communications technologies to enable the ATO to identify and block suspicious activity in real time;

for a new compliance taskforce to recover lost revenue and intervene when attempts to obtain fraudulent refunds are made; and

to improve the ATO’s management and governance of its counter-fraud activities, including improving how the ATO assists individuals harmed by fraud.

Expanding the scope of Part IVA

The Government previously announced in the 2023/24 Budget that it would expand the scope of Part IVA of the ITAA 1936 (the general anti-avoidance rule for income tax) so that it can apply to:

schemes that reduce tax paid in Australia by accessing a lower withholding tax rate on income paid to foreign residents; and

schemes that achieve an Australian income tax benefit, even where the dominant purpose was to reduce foreign income tax.

This measure was proposed to apply to income years commencing on or after 1 July 2024. The Government has now announced in the 2024/25 Budget that it will amend the start date of this measure to income years commencing on or after the day the amending legislation receives Royal Assent, regardless of whether the scheme was entered into before that date.

Freezing social security deeming rates

The Government will freeze social security deeming rates at their current levels for a further 12 months until 30 June 2025 to support age pensioners and other income support recipients who rely on income from deemed financial investments, as well as their payment, to manage cost of living pressures.

Tertiary education system reforms

The Government will provide funding to implement the first stage of reforms to Australia’s tertiary education system. Of note, this includes funding:

- to limit the indexation of the Higher Education Loan Program (and other student loans) debt to the lower of either the Consumer Price Index or the Wage Price Index, effective from 1 June 2023, subject to the passage of legislation; and

- to establish a new ‘Commonwealth Prac Payment’ of $319.50 per week (benchmarked to the single Austudy rate) from 1 July 2025 for tertiary students undertaking supervised mandatory placements as part of their nursing (including midwifery), teaching or social work studies. This will help alleviate the significant financial impact of mandatory placements and increase retention in courses for careers in sectors experiencing shortages.